How A K-Shaped Economy Shapes Grocery Shopping

Since the pandemic ended, consumers have been adjusting to a cost-of-living crisis. With food among the top three essentials, rising grocery prices have pushed shoppers to make more deliberate choices that balance hunger, health, and emotional needs. For instance, in the UK, food prices are on track to be 50% higher in November than at the start of the cost-of-living crisis.[1] Closer to home, grocery prices have surged by over 30% since 2019.[2] Adding to the strain, consumers are encountering the impact of the war in the Middle East. To their credit, Canada’s major grocery chains have declined price increase requests from suppliers. Canadians’ top concern (46%) remains rising food prices.[3]

The prolonged cost-of-living crisis and widening wealth gap have fueled speculation about a pronounced K-shaped economy in Canada. However, CIBC Economics suggests there is less evidence of this pattern, as spending has remained relatively similar across lower-, middle-, and higher-income groups. [4] Yet, as suggested by Mr. A. Grantham, Senior Economist at CIBC, “this won’t be able to last forever, and there is a risk that spending among lower/middle income groups will slow if the improvement seen recently within the labour market doesn’t persist.”[5] For the first four months of the year, Canada shed 112,000 jobs.[6] So, how does a K-shaped economy play out in grocery aisles?

Beyond income polarization, a third force is re-shaping grocery aisles, the GLP-1 weight loss drug. About 15% of Canadians currently use this medication[7], and it is affecting sales of snacks, baked goods, sugary beverages, and alcohol.

What is a K-Shaped Economy?

A K-shaped economy describes a situation where different income groups recover or perform in sharply diverging ways, forming the two arms of the letter “K.” The upper arm of the K (going up): higher-income households with continued spending power. The lower arm of the K (going down): lower- and middle-income households burdened with high costs of living and heavier debt loads.

Is Canada Experiencing a K-Shaped Economy?

While economists are divided on whether Canada is experiencing a K-shaped economy, several signs suggest it is:

- Consumer insolvencies – a measure that indicates how many Canadians filed for relief under the Bankruptcy and Insolvency Act reached a record high (37,121) for the first 3 months of the year.[8]

- Canadian households have reached the breaking point. As part of their most recent study (2026), the Harris & Partners survey revealed:

- 9% of Canadian households live pay-cheque to pay-cheque.

- 9% cutting back on essentials such as heating and groceries.[9]

- Food bank visits are up in 2026 compared to the first four months of 2025.[10] In 2025, food bank usage exceeded 25M visits.[11]

What is the Income Cut-Off line in a K-Shaped Economy?

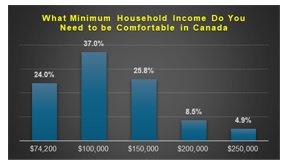

While there is no official income cutoff in a K-shaped economy, a MoneySense and Leger Marketing survey found that 37% of Canadians believe a household income above $100,000 is the minimum needed to feel comfortable. The next largest group, 25.8%, chose incomes above $150,000.[12] Refer to Appendix 1.

How Much Does Each Income Group Spend on Groceries in a K-Shaped Economy?

In a K-shaped economy, lower-income Canadian households typically spend $150-$250 a week and often depend on deep-discount stores, making careful basket-by-basket choices. Higher-income households generally spend $300-$500 a week[13] and have more freedom to buy premium products and shop with greater flexibility.

How is the K-Shaped Economy Playing Out in the Grocery Aisles?

The K‑shaped economy is pushing food retailers to serve two very different sets of economic values as the middle disappears. Higher-income households are accounting for an increasing share of grocery spending. They are shifting more of their spending to warehouse clubs and typically buy fresh foods, vegetables, and meat.

Yet, for the first 3 months of the year, 64% of Canadians earning $100,000 or more indicated they’ve switched to cheaper products in the past year, and 31% say they started buying in bulk to reduce per-item costs.[14] In contrast, lower-income households focus on shelf-stable products and rely heavily on promotions, price tracking, and private-label items to make their budgets go further.

How Can Brands Win in a K-Shaped Economy?

In a K-shaped economy with widening spending gaps, CPG brands must re-think pricing, value, and channel strategy to appeal to both affluent and budget-conscious grocery shoppers. Brands that treat the consumer as a single middle will struggle. The middle is shrinking. Growth comes from clarity about which need state you are serving at each moment of the consumer’s discovery journey. To succeed, CPG brands must serve both ends of the market: premium offerings for higher-income shoppers and strong value options for consumers under tighter budget pressure. Brands must be Authentic and Transparent. Clearly communicate how your brand values align with your customers’ personal identity.

Food Distribution Guy’s Final Thoughts

Much has been said about the K-shaped economy brands are navigating. I would argue that brands and retailers must now respond to an E-shaped economy: the upper arm represents higher-income households, the lower arm lower-income households, and the middle arm Ozempic weight loss drug households.

The K-shaped economy has not ended; it remains a defining feature of the post-pandemic landscape. At the same time, Ozempic-using households are becoming a growing competitive force for brands and retailers.

Navigating a divided market takes more than instinct — it takes strategy. If you’re a CPG brand or retailer looking to connect with the right consumer at the right moment, let’s talk.

APPENDIX 1

References:

[1] UK Food Prices on Track to Rise by 50% Since Start of Cost of Living Crisis, www.theguardian.com. May 2026

[2] AI Overview, May 2026

[3] Winning When Growth is Harder, Carman Allison, Nielsen IQ, May 2026

[4] Is No “K” Ok for Canada, www.ecomics.cibscm.com, January 2026

[5] Canada, U.S. Divergence on Consumer Spending Cause for Concern: CIBC, www.investmentexecutive.com

[6] Stats Canada Labour Force Survey, May 2026

[7] Winning When Growth is Harder, Carman Allison, Nielsen IQ, May 2026

[8] Canada Insolvencies Highest Since 2009 as Canadians Struggle with Debt, www.globalnews.ca, May 2026

[9] Survey Reveals Canadians Have Reached Breaking Point: Harris & Partners, www.retail-insider.com, May 2026

[10] AI Overview, May 2026

[11] Winning When Growth is Harder, Carman Allison, Nielsen IQ, May 2025

[12] Here’s What a Comfortable Income Looks Like in Canada, www.moneysense.ca, September 2025

[13] AI Overview, May 2026

[14] 64% of Wealthy Canadians Say They’ve Switched to Cheaper Products in the Past Year, Omnisend, www.retail-insider.com, February 2026